By Adnan Adams Mohammed

As Ghana’s banking sector transitions from a period of defensive survival to one of calculated expansion in early 2026, the Agricultural Development Bank (ADB) PLC is emerging as one of the industry’s strongest performers. At the center of this resurgence is what analysts have described as the bank’s “Fortress Liquidity” a robust financial cushion that places it among the most resilient institutions in the country.

Recent industry data and financial disclosures point to a banking sector steadily recovering from the shocks of macroeconomic instability. Within this improving environment, ADB stands out as a key beneficiary, leveraging strong liquidity levels to position itself for the next phase of growth.

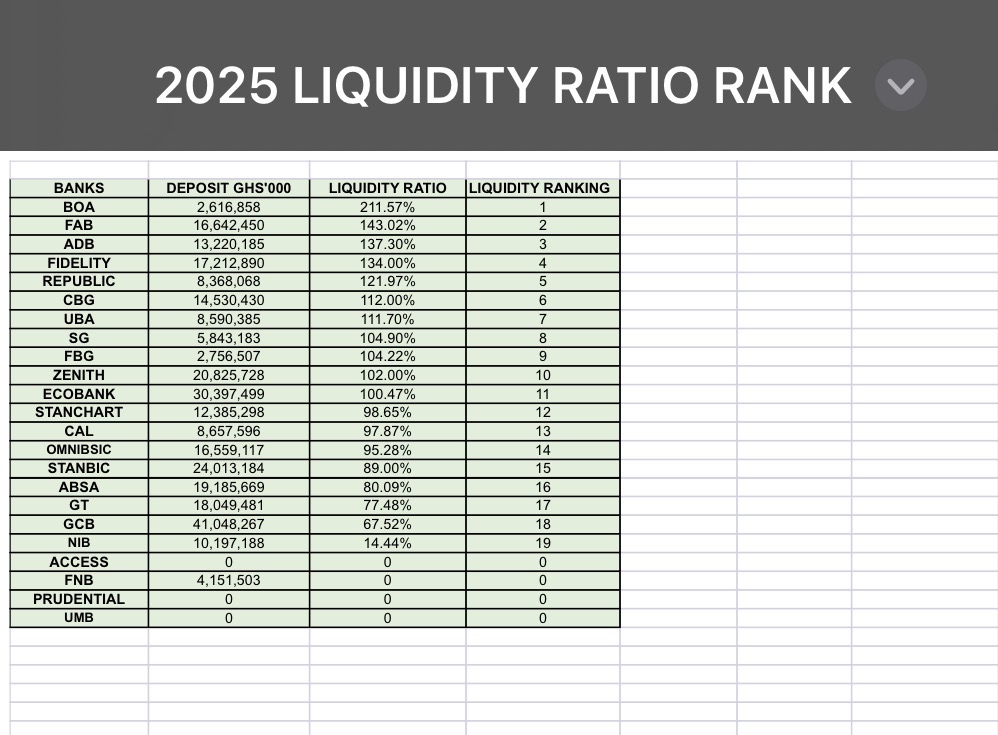

A comparative review of banks’ financial statements shows that ADB is outperforming several major competitors in its ability to meet short-term obligations. While the industry’s Core Liquid Assets to Total Assets (CLATA) averaged 26% by the end of 2025, ADB’s individual liquidity profile tells a more aggressive story of capital preservation and balance sheet strength.

With a liquidity ratio of 137.30%, ADB ranks third among top-tier banks. It trails only Bank of Africa (211.57%) and FAB (143.02%), but still holds a competitive edge over larger institutions such as Fidelity Bank (134.00%) and Zenith Bank (102.00%). This strong positioning underscores ADB’s ability to maintain a significant buffer against financial shocks while remaining competitive in a tightening market.

The broader banking industry is also showing clear signs of recovery. By March 2026, key financial soundness indicators including liquidity, solvency, and operational efficiency were all trending upward, according to central bank assessments.

Liquidity continues to serve as the foundation of this recovery. By the close of 2025, the industry’s Core Liquid Assets to Short-Term Liabilities (CLASTL) stood at approximately 33%, reinforcing banks’ ability to meet immediate obligations.

At the same time, asset quality is improving. The Non-Performing Loan (NPL) ratio declined to 18.7% in February 2026, down from 22.6% the previous year a signal that banks are gradually overcoming the credit stress experienced during recent economic turbulence.

To sustain these gains, regulators have introduced stricter liquidity monitoring frameworks aligned with Basel III standards. These measures are designed to ensure that banks remain resilient even in the face of renewed market volatility.

ADB liquidity ratio has improved from 125.55% in late 2024 to current levels, creating a substantial safety buffer well above regulatory requirements. At the same time, ADB’s total asset base has expanded to approximately GH₵16.20 billion as of September 2025.

Equally important is the bank’s clean regulatory record, having reported zero statutory breaches a reflection of improved governance and compliance discipline.

With returns on government securities gradually declining evidenced by 91-day Treasury bill rates easing to around 27.7% banks are being pushed to rethink their strategies.

For ADB, this means a deliberate pivot toward private sector lending. The bank’s 2026 strategy is built around two primary pillars:

First, expanding credit to the agribusiness sector. By targeting the agricultural value chain, ADB aims to generate higher margins while supporting a critical segment of the economy.

Second, accelerating digital transformation. Investments in digital payment systems are expected to reduce operational inefficiencies that previously weighed on the bank’s performance, particularly in 2024.

Climate-related shocks remain a major concern. In recent periods, such challenges have already slowed agricultural growth to 5.7%. Should similar conditions persist or worsen in 2026, there is a risk of rising loan defaults, which could put pressure on asset quality.

This is particularly relevant as the industry continues to recover from elevated NPL levels, even though recent improvements offer some reassurance.

ADB enters the second quarter of 2026 in one of its strongest financial positions in years. Its “Fortress Liquidity” provides a solid shield against uncertainty, but the real test lies ahead.

The bank’s success will ultimately depend on how effectively it channels its liquidity into productive lending, particularly within the private sector, without compromising credit quality.