Gold dominated global markets in 2025, with prices surging more than 40% over the year their strongest annual performance since 1979 and setting fresh records more than 50 times. The rally rewarded not only investors in bullion but also mining companies, many of which posted record cash flows and soaring valuations.

The world’s largest gold-mining exchange-traded fund (GDX) climbed more than 155% in 2025, far outpacing the metal itself. Across Canada’s TSX, gold miners dominated the list of top-performing stocks.

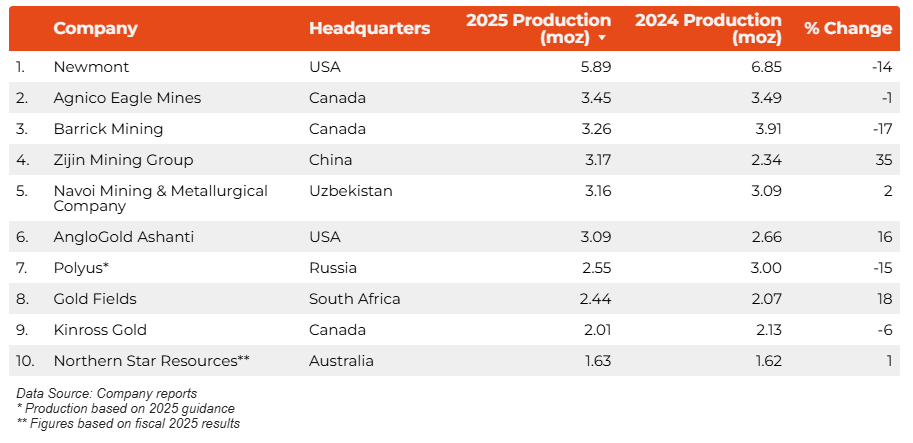

Still, strong gold prices were only part of the story. Operational performance, asset acquisitions, geopolitical challenges and expansion plans also shaped how the world’s biggest producers fared during the year.

Newmont retained its position as the world’s largest gold producer following what it described as a “record year” for cash generation. The Denver-based miner achieved several milestones, including the commercial start of its Ahafo North project in Ghana, while divesting non-core assets to streamline operations. Although Newmont met its annual production guidance, output declined 14% year-on-year, and the company has signaled a further drop in 2026.

Canada’s Agnico Eagle Mines climbed into second place after delivering production above the midpoint of its 2025 guidance range. The miner strengthened its portfolio with key investments, including the acquisition of O3 Mining and equity stakes in Perpetua Resources and several junior explorers. The company expects stable production over the next three years, supported by significant resource growth and record-high reserves.

Barrick Gold endured a turbulent year, largely due to setbacks in Mali. Operations at its Loulo-Gounkoto complex were suspended in January amid a dispute with the country’s military government, and operational control was temporarily lost. The dispute was resolved in December, allowing production to resume. Despite the recovery, the disruption contributed to a sharp decline in overall output.

China’s Zijin Mining Group moved into fourth place after reporting a 35% increase in gold production year-on-year. The growth was driven by operational efficiency and strategic acquisitions, including the Akyem mine in Ghana from Newmont and the Raygorodok mine in Kazakhstan, as the company continues expanding into Central Asia.

Uzbekistan’s Navoi Mining and Metallurgy Company maintained steady output growth in 2025. Its flagship Muruntau deposit, one of the world’s largest gold mines, anchors operations across the Kyzylkum Desert. The company estimates it holds around 150 million ounces of gold in resources.

AngloGold Ashanti became a three-million-ounce producer in 2025, helped by the first full-year contribution from Egypt’s Sukari mine following its takeover of Centamin in 2024. The company also expanded its North American footprint through the acquisition of Augusta Gold, adding assets in Nevada.

Russia’s Polyus projected production of between 2.5 million and 2.6 million ounces for 2025, slightly lower than the previous year due to a planned reduction at its Olimpiada mine. Like other major Russian producers, the company continues to face Western sanctions that have impacted parts of its operations.

South Africa’s Gold Fields recorded an 18% rise in production in 2025, driven by improved performance across its portfolio and the commercial start of the Salares Norte mine in Chile. The company also strengthened its Australian presence through a A$3.7 billion takeover of Gold Road Resources and has indicated it remains open to further acquisitions.

Kinross Gold once again delivered more than two million ounces in gold-equivalent production, despite declines at some sites. Higher grades at its Paracatu mine in Brazil and Fort Knox in Alaska boosted overall output. The company expects similar production levels in 2026 and plans significant investment in three U.S. development projects.

Australia’s Northern Star Resources met its 2025 fiscal-year guidance, supported by strong performance at its KCGM operations. During the year, it completed a A$5 billion acquisition of De Grey Mining, a deal that could lift annual production to as much as three million ounces. However, the company has slightly lowered its fiscal 2026 guidance due to isolated operational events late in 2025.

With gold prices at historic highs and investor appetite strong, 2025 proved to be a landmark year for the world’s biggest gold miners. Yet sustaining that momentum will depend not only on bullion prices but also on operational discipline, geopolitical stability and strategic expansion in the years ahead.